- Solutions

ENTERPRISE SOLUTIONS

Infuse new product development with real-time intelligenceEnable the continuous optimization of direct materials sourcingOptimize quote responses to increase margins.DIGITAL CUSTOMER ENGAGEMENT

Drive your procurement strategy with predictive commodity forecasts.Gain visibility into design and sourcing activity on a global scale.Reach a worldwide network of electronics industry professionals.SOLUTIONS FOR

Smarter decisions start with a better BOMRethink your approach to strategic sourcingExecute powerful strategies faster than ever - Industries

Compare your last six months of component costs to market and contracted pricing.

- Platform

- Why Supplyframe

- Resources

Semiconductor and chip shortages have had an adverse effect on almost every industry that deals in any form of electronics. With the automotive industry introducing new EVs and autonomous features in recent years, cars have become more complex from a technological standpoint than ever before.

That is why the automotive industry is feeling immense pressure from the shortages, leading to drastic cuts in output, a sharp increase in used vehicle prices, and even missing features from upcoming models. As an organization that works with both the buy and sell side of the global electronics value chain, Supplyframe has been reporting on this evolving situation for some time now. With no end in sight, it’s time to examine the state of the shortages, and unveil new data from our global DSI Network.

The State of Component Shortages

With Supplyframe data indicating that the current shortages could last into the first quarter of 2023, automotive supply chains are already being forced to rethink their standard approaches. A recent interview with several automotive executives conducted by Auto News revealed a mixture of optimism and ongoing uncertainty.

“We’re seeing a positive trend, but of course it’s very dynamic, and we can’t predict the future.”

Robert Young, Group VP, Purchasing Supplier Development at Toyota Motor North America

The consensus among the executives was that starting and stopping production is the largest concern. The current focus is to keep things stable moving forward, and exploring new forms of collaboration with suppliers.

Meanwhile, automakers are having to make more and more difficult decisions in the name of maintaining stability in the supply chain. General Motors recently announced that they will be forced to remove automatic start-stop systems from their full-size pickups and SUVs produced by their brands, simply because they cannot source the chips required to power the technology.

This has led General Motors to take a step back and commit to making major changes to their supply chain in the wake of the continued shortages. The Detroit-based carmaker has said they will make “substantial shifts” in the supply chain by “building direct relationships with manufacturers.”

General Motors CEO, Marry Barra, said in a discussion with Delta Air Lines Inc. CEO, Ed Bastian, that “it’s a solvable problem, but it’s going to be here a little longer.” She went on to acknowledge that the semiconductor shortage is a reflection of the unique landscape of the global economy during the pandemic, combined with decisions the industry made in the early days of the health crisis.

The challenges also come from shifts in demand, as consumers expect more and more technology incorporated into automotive designs, which drives the chip requirements per vehicle upward as well. This demand also shifted drastically in 2020, rising far higher than manufacturers had predicted as lockdowns began to lift in certain parts of the world.

All of this is leading towards smarter collaboration with suppliers like Intel Corp., Qualcomm Inc., and Nvidia Corp., with a focus on more closely monitoring supply levels.

Despite the shortages, these new avenues of demand from sources like the automotive industry will be a boon to the semiconductor market in the long term. IDC expects the semiconductor market to grow by 17.3% in 2021, compared to 10.8% in 2020. Interestingly, as part of their findings, the IDC also claimed that there would be a potential overcapacity of inventory by 2023 as new expansions to global capacity come online by the end of 2022.

The Supplyframe Perspective: New Data From The DSI Network

Supplyframe’s Design-to-Source Intelligence (DSI) Network gathers billions of data points from over 70 web properties and over 10 million engineering and sourcing professionals to paint a complete picture of the global electronics value chain.

Below is a combination of data that we have been tracking since January of 2020 surrounding the automotive industry, chip shortages, and seminconductor production for microcontroller units (MCUs). This data reflects overall demand, price, stock, and the percentage of MCU components out of stock on any given month.

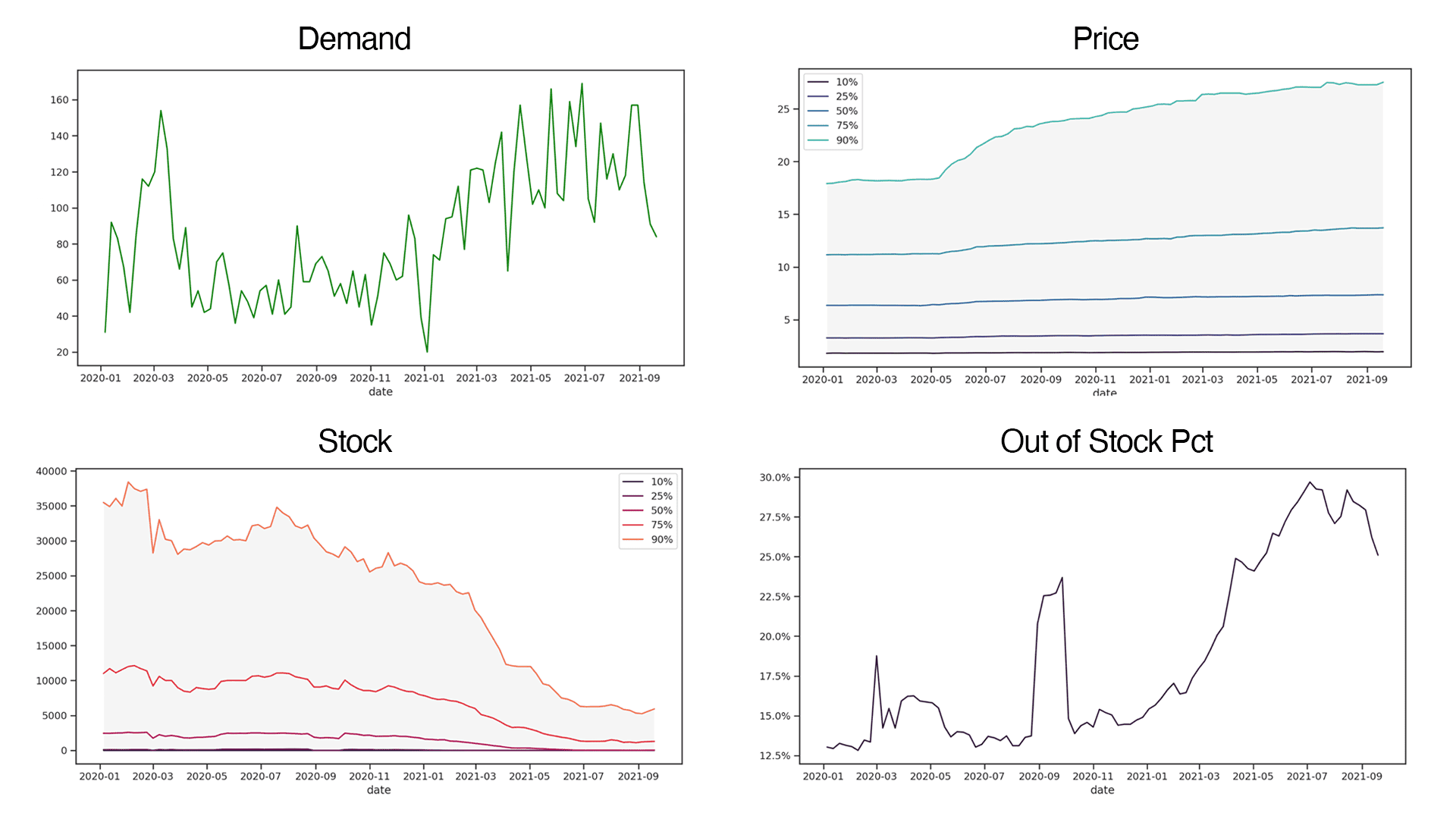

Automotive

Beginning with Automotive MCUs, we can see demand data in the top left that shows a drop throughout the middle of 2020, but as we move towards the holiday season of 2020 and into 2021, demand continues to rise drastically. Meanwhile, the stock graph just below illustrates a sharp drop in availability during the same time period.

Shifting to the right side of the graphs, prices in the 90th percentile at the top of the graph show a major spike in the middle of 2020, while others show a steady increase. All of this data is correlated once more in the out of stock percentage graph in the bottom right. Together these four graphs paint a clear picture of what industry professionals refer to as a “perfect storm” of factors that led to the chip shortages.

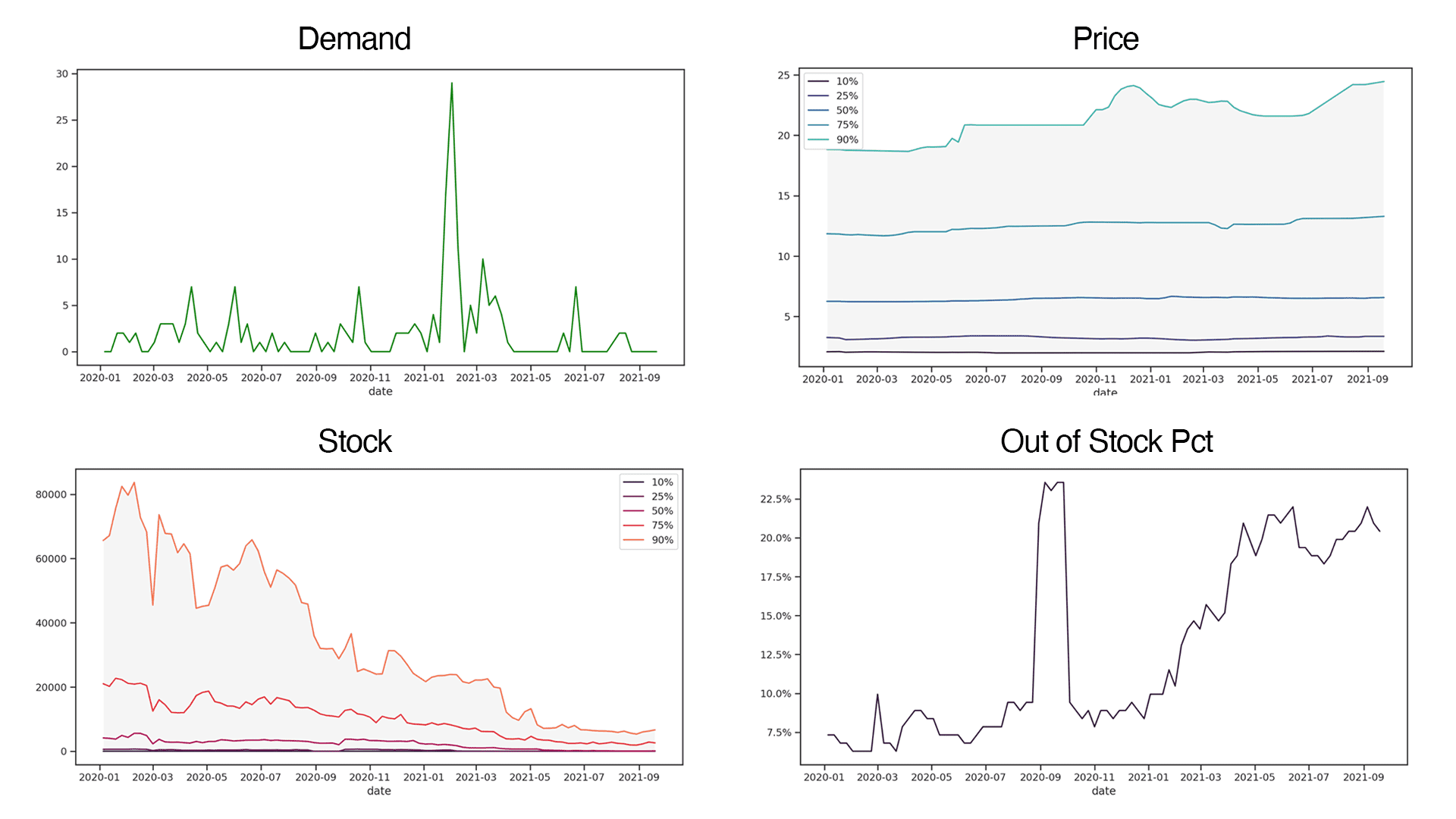

Semiconductors

If we pull the scope outward and look at Supplyframe data surrounding semiconductors for MCUs, we can see a massive spike in demand on the upper-left graph in the first quarter of 2021. Both the available stock and percentage of out of stock components saw similar effects in the same time period. Meanwhile, pricing shows fluctuations throughout the end of the 2020 and into 2021.

This data revealed potential spikes in demand and reduced stock several months before the shortages took hold. How would access to this data have changed your organization’s approach to the emerging shortages? Leveraging this kind of data in real-time could have mitigated some of the risk, delays, and costs associated with the current instability in the automotive supply chain.

Earlier in 2021, we introduced Supplyframe Commmodity IQ, a brand new solution that allows subscribers to access valuable data surrounding subcommodity groups, much like the data you see above. Access to CommodityIQ provides comprehensive insights into demand, pricing, availability, and emerging trends across everything from raw materials to semiconductors, MCUs, and much more.

CommodityIQ provides the kind of data and insights you won’t find anywhere else, powered by our DSI Network, industry partners, and expert analysis. A subscription allows organizations to stay ahead of the curve, mitigating risk before it becomes a larger issue. Even as a subscriber, however, shortages will continue, so the question remains: is there any relief on the horizon?

A Light at The End of The Tunnel?

The good news is that automakers are seeing the value in bringing more collaboration and visibility into their supply chains. Global efforts are also underway to ensure that capacity increases, which brings its own potential developments for the future.

In early September of 2021, Intel announced they will be investing $95 billion into two new chip foundries in Europe over the course of the next decade. Intel CEO, Pat Gelsinger spoke at the IAA Mobility automotive event in Munich recently, opening his talk with the following statement:

“We need you and you need us. This is a symbiotic future that we are off innovating and supplying as the automobile becomes a computer with tires.”

Intel CEO Pat Gelsinger

Gelsinger predicts that the automotive total addressable market for semiconductors will expand from $50 billion as it is today, to $115 billion by 2030, showcasing the exponential rise in demand for these components in current and future automotive designs. This prediction is further elevated by Intel’s substantial investment into growing chip capacity.

Even the U.S. Government is getting involved with chip manufacturing to help alleviate the shortages. The CHIPS for America Act, which passed the Senate earlier in 2021, provides income tax credit for semiconductor equipment or manufacturing facility investments into 2026, adding incentive for companies to further invest into semiconductor manufacturing in the U.S.

This news of investment into capacity and semiconductor manufacturing is welcome indeed, but it comes with its own risks. Specifically, the sheer increase in chip manufacturing over the course of the next year could lead to a “chip flood” in 2023, as capacity overtakes demand. IDC predictions indicate this could lead to significantly decreased prices in 2023 when the scales tip in the opposite direction.

Ultimately, this news is yet another reason why insight and visibility into the global markets is more important than ever. As organizations navigate shortages and look for potential price drops going into 2023, Supplyframe Commodity IQ presents a valuable resource in pinpointing these emerging trends well before your competitors can spot them, leading to smarter decisions, higher margins, and a stronger supply chain as a result.

")